Thu, Apr 18, 2024

23.12°C Kathmandu

23.12°C KathmanduMoney

Credit demand subdued despite rise in stock of loanable fund

Commercial banks have finally managed to replenish the stock of funds that could be immediately extended as loans, providing big relief to bankers who were anticipating a fall in profitability due to inability to disburse credit.

bookmark

Published at : August 10, 2017

Updated at : August 10, 2017 08:24

Kathmandu

Commercial banks have finally managed to replenish the stock of funds that could be immediately extended as loans, providing big relief to bankers who were anticipating a fall in profitability due to inability to disburse credit.

Greater availability of loanable funds may not, however, translate into rise in credit disbursement anytime soon, as lending rates, which had soared during the time when banks were facing credit crunch, are not likely to come down soon. This is expected to prompt borrowers to postpone their investment plans.

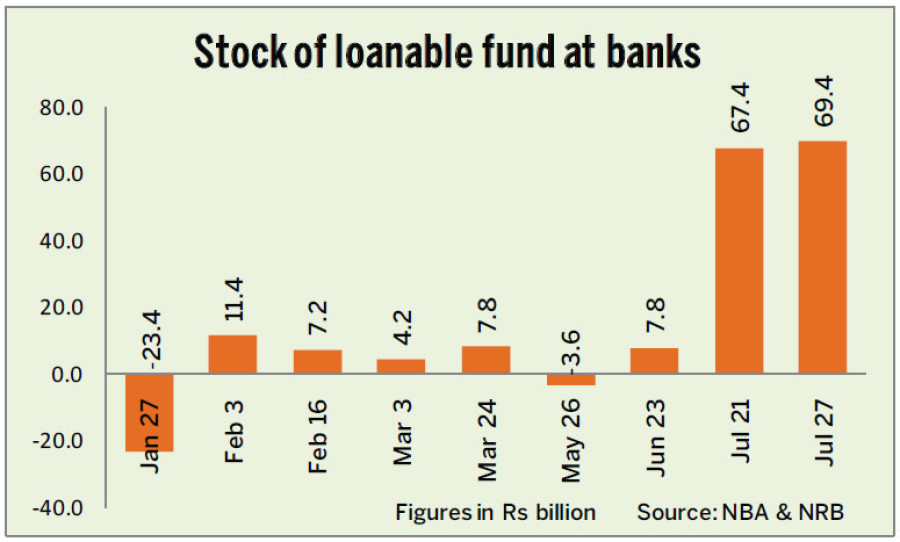

Commercial banks are currently sitting atop loanable fund of around Rs69.4 billion, data compiled by the Post based on statistics of the Nepal Bankers’ Association (NBA) and the Nepal Rasta Banks show.

This is a big turnaround considering the situation of two months ago when commercial banks, in aggregate, did not have an extra penny to convert into loans.

The stock of loanable fund at commercial banks has lately jumped because of surge in deposit collection. Commercial banks drew fresh deposits of Rs146 billion in around 70-day period between May 19 and July 27, show NBA statistics.

Banks have started witnessing greater inflow of deposits as contractors, who worked on behalf of the government in the last fiscal year, started encashing cheques. Also, transfers of around Rs75 billion made by the government to newly-formed local bodies via commercial banks pushed up the level of deposits at financial institutions. On top of that, maturity of one-year NRB Bonds towards the end of last fiscal year injected around Rs31 billion in the banking sector.

All these reasons have pushed up the liquidity level at banks. This, in turn, has also raised the stock of funds that could be immediately extended as loans.

The existing stock of loanable fund is adequate to meet the credit demand of the private sector of at least two months considering the trend of the last fiscal year.

Commercial banks had extended around Rs352 billion in credit to the private sector in the last fiscal year, NBA data show. This means a loan of around Rs29.4 billion was disbursed per month in the last fiscal year.

Banks and financial institutions in the country are allowed to extend 80 percent of the total deposit and core capital as credit. This is referred to as the credit to core capital-cum-deposit (CCD) ratio. This ratio stood at 80.2 percent in the end of May, meaning banks had exceeded the lending limit by 0.2 percentage point.

The CCD ratio of commercial banks currently hovers around 77 percent.

“The improvement in CCD ratio has provided a big relief to us as it enables us to increase credit disbursement,” Nabil Bank CEO Sashin Joshi said.

Yet credit disbursement, according to Joshi, has and will remain subdued in the coming days, as lending rates, which are fixed on the basis of base rates, are quite high and are likely to remain at the higher end in the coming days as well.

The average lending rate of commercial banks surged to 11.3 percent in June, as against 9 percent in the same month a year ago. Average base rate of commercial banks, meanwhile, stood at 9.4 percent in June, in comparison with 6.3 percent in June 2016.

This means commercial bank, on average, added a premium of 1.9 percentage points to the base rate in June to fix the lending rates.

“Many banks may not want to immediately reduce the premium added to the base rate as it will lower effective interest rate and hit profitability in the coming days,” Joshi said. “This indicates lending rates will remain high in the coming days as well.”

Similar opinion was expressed by Laxmi Bank CEO Sudesh Khaling.

“Despite hike in loanable funds, we are still apprehensive about rise in credit disbursement because of high lending rates. As a result, many borrowers are in a wait-and-watch mode,” Khaling said.

Lending rates of banks, according to Khaling, are unlikely to come down any time soon, as many banks had collected fixed deposits at higher rates when the stock of loanable funds had depleted.

“This means demand for fresh credit from the productive sector will remain low in the coming days,” Khaling said.

This has once again raised chances of loans flowing towards unproductive sectors, such as stocks and automobiles.

Recently, the central bank allowed auto loan seekers to purchase vehicles by making a down payment of 35 percent of the value of the vehicle, down from 50 percent in the past. Since the peak season for sales of automobiles—which falls in Dashain-is round the corner, chances of more credit flowing towards auto sector are high.

Most Read from Money

Editor's Picks

E-PAPER | April 18, 2024

×