Thu, Apr 18, 2024

20.12°C Kathmandu

20.12°C KathmanduMoney

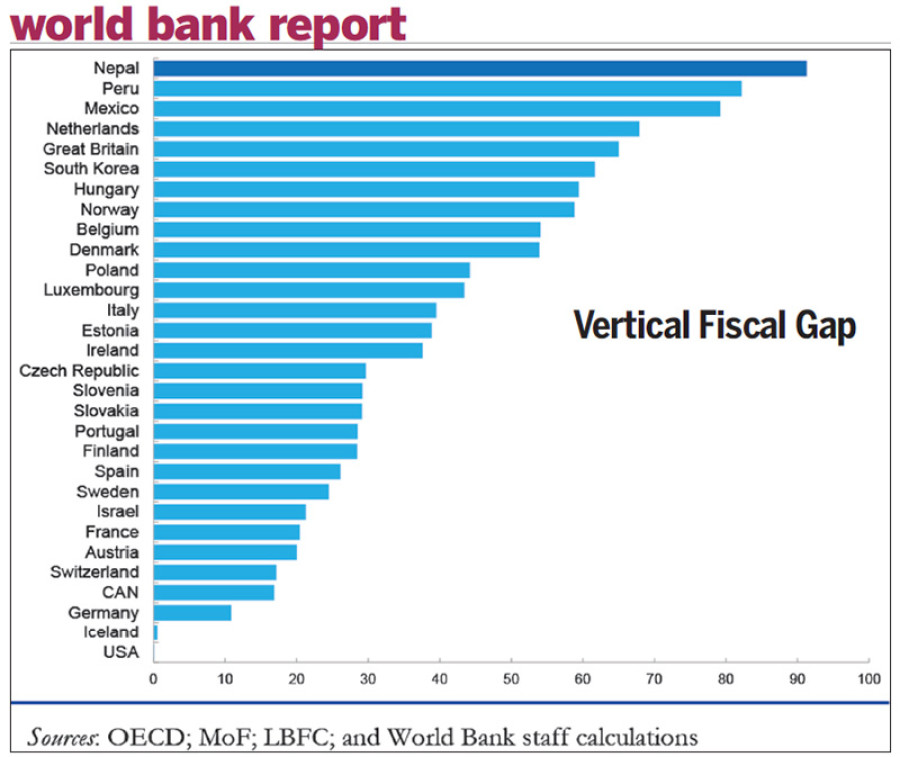

Nepal’s vertical fiscal gap to be widest in federal countries

Many newly-formed local bodies in the country may not be able to deliver public services effectively and efficiently, as they have limited independent income sources to cater to people’s needs, says a latest World Bank (WB) report.

bookmark

Published at : September 20, 2017

Updated at : September 20, 2017 08:39

Kathmandu

Many newly-formed local bodies in the country may not be able to deliver public services effectively and efficiently, as they have limited independent income sources to cater to people’s needs, says a latest World Bank (WB) report.

Nepal has carved out 753 local bodies following adoption of the federal structure as per the provision in the constitution promulgated in September 2015. These local bodies, among others, are responsible for building infrastructure projects, such as roads and irrigation facilities, and providing primary and secondary education, and basic healthcare and sanitation services.

Local people expect local bodies to cater these services in an effective and efficient manner, as they have just elected their local representatives after a gap of around 20 years. But the big problem is many local governments do not have their own sources of income.

Major sources of revenue in the country are value added tax, income tax, and customs and excise duties. All these taxes and duties will be collected by the central government. Local bodies, on the other hand, will be allowed to collect property, house rent, real-estate registration, vehicle, land, entertainment, advertisement, business and hoarding board taxes, which make very little contribution to the total government revenue.

This income generation arrangement, according to the World Bank, implies tax collection in federal Nepal will not be significantly different from the unitary system, as approximately 80 to 85 percent of the total revenue is likely to remain with the central government. This means sub-national taxes will account for less than 1 percent of the gross domestic product, and are likely to represent less than 2 to 3 percent of total general government revenue.

This combination of centralised tax collection and decentralised service provision creates vertical fiscal gap, says the Special Report on ‘Fiscal Architecture for Federal Nepal’ published in WB’s latest edition of the Nepal Development Update. And Nepal’s vertical fiscal gap is likely to be one of the largest among federal countries because of very little contribution of sub-national governments in total revenue generation.

Although it is difficult to determine the optimal vertical fiscal gap for each federal system, recent empirical studies indicate that incentives for expenditure efficiency are reduced when fiscal gaps are very large, or when sub-national own-source revenues are very low, adds the report.

In addition to vertical imbalances, large disparities in socioeconomic development are expected to create “so-called horizontal imbalances” as well.

Currently, per capita revenue generated by Kathmandu district through its own sources is 10 times higher than in Darchula district. This will continue in the federal context too, creating horizontal fiscal gap, says the WB report.

To bridge the vertical and horizontal fiscal gaps, the government has proposed to extend 15 percent of the income generated from VAT and excise duties imposed on domestic products to local bodies. The government has also proposed to extend 5 percent of the royalty generated from use of natural resources, namely mountains, hydropower, forests, and mines and minerals, to local bodies. On top of these, the government has also proposed to extend four grants-fiscal equalisation, conditional, matching and special-to local bodies.

But transfers can also weaken fiscal discipline, as sub-national governments and their creditors may expect the central government to bear the ultimate responsibility for deficits and debt, says the report. “Finally, limited revenue autonomy reduces the ability of sub-national governments to implement fiscal adjustments, because in the absence of revenue side measures, spending cuts are their only available policy instrument.”

The WB report does not make any concrete suggestion on ways to address this

problem. But it says: “Consumption or indirect tax bases are typically the most important sources of state and local tax revenue, but in Nepal these sources are exclusively listed in the schedules of the central government in the constitution, while sub-national governments are left with the authority to levy taxes with small bases.”

The report further says: “While centralised tax collection combined with transfers to sub-national governments can maximise efficiency on the revenue side, increasing own-source revenue collection by sub-national governments can promote expenditure efficiency by improving accountability and strengthening taxpayer oversight.”

Most Read from Money

Editor's Picks

E-PAPER | April 18, 2024

×